Economics

(214)

Q1. Economics is science of scarcity and choice. Explain.

Ans. Scarcity refers to the finite nature and availability of resources while choice refers to people’s decisions about sharing and using those resources. The problem of scarcity and choice lies at the very heart of economics, which is the study of how individuals and society choose to allocate scarce resources

Q2. Differentiate between micro and macroeconomics?

Ans. Microeconomics is the study of economics at an individual, group, or company level. Whereas, macroeconomics is the study of a national economy as a whole. Microeconomics focuses on issues that affect individuals and companies. Macroeconomics focuses on issues that affect nations and the world economy.

Q3. Distinguish between economic and non-economic wants.

Ans.

| ECONOMIC ACTIVITY | NON-ECONOMIC ACTIVITY |

| Economic activity refers to a human activity related to production and consumption of goods and services for economic gain. | Non-economic activity is an activity performed gladly, with the aim of providing services to others without any regard to monetary gain. |

| Economic, i.e. to earn money. | Social or psychological, i.e. out of love, affection, etc. |

| Creation of wealth and assets. | Satisfaction and happiness. |

Q4. Why should we limit our wants?

Ans. As we all know our wants are unlimited but our resources to satisfy these wants are limited. Hence if we keep our wants as unlimited and growing, we will not be able to satisfy all of them with our limited resources. This will give rise to a lot of dissatisfaction.

Therefore, we should limit our wants so that we can satisfy most of them with our limited resources and this will give us more and more satisfaction.

Q5. How do the resources satisfy the wants.

Ans. Resources is a source that is generate form nature. the resources satisfy the wants because is the will no resource like – chair, table, food (that we cook) etc. we can’t survive in this world. some examples for reading in school tables, chair are made form wood, which is a source. the clothes that we ware this is made of cotton, wool, silk etc. that is a source.

so, my dear friend only the resource can only satisfy the human needs.

Q6. What is meant by an economy? Give the major characteristics of a capitalist economy.

Ans. The meaning of economy is the careful management of available of resources

Main features of capitalist of economy

- Private property

- having of freedom of enter prices

- Soverginity of the consumer

- No government interference

- improving profit motive

Q7. What are the main functions of an entrepreneur?

Ans. The following points highlight the top five functions of an entrepreneur. The functions are:

- Decision Making

- Management Control

- Division of Income

- Risk-Taking and Uncertainty-Bearing

- Innovation.

Q8. Distinguish between sole proprietorship and partnership.

Ans.

| Sole Proprietorship | Partnership |

| In Sole Proprietorship, there is only one owner, he has all the right of decision-making for the business and has to perform all the management work alone. | The Partnership is one of the types of business in which two or more persons/businesses make a formal agreement between them of sharing business ownership, profits/Losses, responsibilities, and duties of the business |

| There is only one minimum number of members is required. | There are two minimum numbers of members are required. |

| All profit is enjoyed by the owner only and all loss will bear by the owner. | All profit is distributed as per the partnership agreement (partnership Deed). |

| This type of business is managed by only one person. It means by is the owner. | his type of business can be managed by all the partners |

Q9. Distinguish between private sector and public sector production units.

Ans.

| PUBLIC SECTOR | PRIVATE SECTOR |

| The section of a nation’s economy, which is under the control of government, whether it is central, state or local, is known as the Public Sector. | The section of a nation’s economy, which owned and controlled by private individuals or `companies is known as Private Sector. |

| To serve the citizens of the country. | Earning Profit |

| Job security, Retirement benefits, Allowances, Perquisites etc. | Good salary package, Competitive environment, Incentives etc. |

Q10. Distinguish between sole proprietorship and partnership.

Ans.

| SOLE PROPRIETORSHIP | PARTNERSHIP |

| A type of business organization, in which only one person is the owner as well as operator of the business is known as Sole Proprietorship. | A business form in which two or more persons agree to carry on business and share profits & losses mutually is known as Partnership. |

| Business secrets are not open to any person except the proprietor. | Business secrets are open to each and every partner. |

| Scope for raising capital is limited. | Scope for raising capital is comparatively high. |

Q11. Give the difference between fixed and variable cost?

Ans.

| Fixed cost | Variable cost |

| Fixed cost is referred to as the cost that does not register a change with an increase or decrease in the quantity of goods produced by a firm. | Variable cost is referred to as the type of cost that will show variations as per the changes in the levels of production. |

| It is time-dependent and changes after a certain period of time. | It is volume-dependent and changes based on the volume produced. |

| Rent, salaries, and property taxes | Labour cost, cost of raw materials, and sales commissions |

Q12. Define demand. Distinguish between individual demand and market demand.

Ans. Demand is the quantity of consumers who are willing and able to buy products at various prices during a given period of time. Demand for any commodity implies the consumers’ desire to acquire the good, the willingness and ability to pay for it.

| Basis of Difference | Individual demand | Market demand |

| Represents | It represents the quantities demanded, at different prices, by an individual. | It represents the aggregate quantities demanded at different prices, by all the consumers. |

| A shape of curve | The individual demand curve is relatively steeper | The market demand curve is relatively flatter. |

Q13. What is a demand curve? Draw an individual demand curve with the help of a hypothetical demand schedule.

Ans. Demand curve is a graphical representation of demand schedule. It is the locus of all the points showing various quantities of a commodity that a consumer is willing to buy at various levels of price, during a given period of time, assuming no change in other factors.

Q14. Why does the demand curve slope downwards from left to right?

Ans. When the price of commodity increases, its demand decreases. Similarly, when the price of a commodity decreases its demand increases. The law of demand assumes that the other factors affecting the demand of a commodity remain the same.

Thus, the demand curve is downward sloping from left to right.

Q15. Define supply. Distinguish between individual supply and market supply.

Ans. The fundamental economic concept that states the total amount of a specified product or service that is available to customers is known as ‘supply.’ It is very closely related to and goes hand in hand with demand. When supply exceeds demand for a product or service, the prices of said product fall. This is known as the law of supply and demand. Their relationship highly affects the price of goods and is a very important topic in the field of economics.

| Individual Supply | Market Supply |

| It refers to the quantity of commodity supplied by a single seller. | It refers to the quantity of a commodity supplied by all the sellers or the firms in the market. |

| Individual supply is a component of Market supply. | It is the aggregation of individual supply. |

Q16. Why does the supply curve slope upwards?

Ans. Decisions to supply are largely determined by the marginal cost of production. The supply curve slopes upward, reflecting the higher price needed to cover the higher marginal cost of production. The higher marginal cost arises because of diminishing marginal returns to the variable factors.

Q17. State and explain the law of supply using a suitable numerical example.

Ans. The ‘law of supply’ states that ‘Other things remaining same, the supply of a product rises as Its price rises and falls as its price falls’.

Suitable numerical example is

Price (Rs) Quantity supplied.

6.00 3000

7.00 4000

8.00 5000

9.00 6000

It shows the supply of commodity at all different prices. At price Rs, 6.00 per unit 3000 units of x are supplied and at price Rs 7.00 the supply increases to 4000 and so on. It is observed that bigger quantities are offered at a ‘higher price’ than at a ‘lower price.’

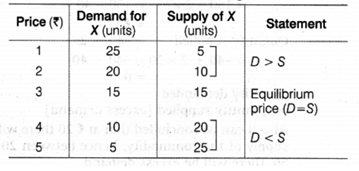

Q18. How is equilibrium price of a commodity determined?

Ans. The equilibrium price is the price at which market demand and market supply are equal to each other as shown in following schedule and diagram:

When price is Rs. 5, the supply of commodity X is 25 units. With a view to increase their sales, the seller will reduce the price. At Rs. 3 demand and supply of commodity X becomes equal’to 15. Hence, Rs. 3 is the equilibrium price.

In the given figure, demand and supply of commodity Z are equal at E point. Equilibrium price is OP at Rs.3. If market price is Rs 4, the demand will be (10) less than supply (20), excess supply will force the market price to slide down till the equilibrium between supply and demand is struck. Thus, equilibrium price will be restored in the free market economy.

Q19. How is equilibrium price of a commodity affected when demand increases

but supply remains the same.

Ans. Equilibrium means a state of balance where there is no tendency to change. The forces determining equilibrium relating to the price are the balance between the quantity demanded and quantity supplied of the commodity. The price at which quantity demanded of a commodity is equal to its quantity supplied of that particular commodity is called the equilibrium price.

When demand for a particular commodity increases but supply remains the same then both equilibrium price and quantity demanded and supplied will increase.

Q20. Define Perfect Competition.

Ans. Perfect competition is a type of market where there are many buyers and sellers, and all of them initiate the buying and selling mechanism. There are no restrictions and no direct competition in the market. It is assumed that all the sellers are selling identical or homogenous products.

Q21. Define Monopoly.

Ans. Monopoly is a situation where there is a single seller in the market.

In conventional economic analysis, the monopoly case is taken as the polar opposite of perfect competition. By definition, the demand curve facing the monopolist is the industry demand curve which is downward sloping. Thus, the monopolist has significant power over the price it charges, i.e. is a price setter rather than a price taker.

Q22. Explain the features of Perfect Competition and Monopoly.

Ans. Perfect competition – One of the main features of perfect competition is that all producers contribute significantly to the market. Their production and supply levels do not change the curve. All of these producers are price takers. They do not influence the market. If any company or firm tries to raise its prices, the consumer would instead buy from a competitor at a lower price.

Monopoly – Only One Seller and Various Buyers. The major characteristics of the monopoly are to own one seller and various buyers.

Q23. How do taxes and subsidies affect the market price of a commodity?

Ans.

- When there is a government subsidy, the price the government offers is ussually lower, thereby the market price of that commodity shall drop.

- When the government cuts taxes on a commodity, the price of that particular product shall rise.

- when the government raises taxes, then the price of the commodity shall rise

Q24. What is token price? What is the purpose behind fixing token price of a commodity?

Ans. Token price refers to a price which is far below the cost of production per unit of goods and services.

Certain section of the population cannot afford to avail certain essential goods and services at their market price. These essential goods and services includes education services, health services and medical services, To overcome this issue Government as well as few privately owned ‘Charitable Institutions’ provide the underprivileged section of the population with these services at a token price.

The main purpose behind fixing token price of a commodity is to prevent its wasteful use and provide these goods and services to the genuine end user.

Q25. What is control price? How does it affect the consumers?

Ans. Price controls are government-mandated legal minimum or maximum prices set for specified goods. They are usually implemented as a means of direct economic intervention to manage the affordability of certain goods.

Standard economic theory predicts that new policies that reduce industry competitiveness and add substantially to business and industry costs will likely lead to higher consumer prices, reduced quantity of products and services and, perhaps, reduced quality and fewer choices for consumers.

Q26. Distinguish between health and life insurance?

Ans.

| Life insurance | Health insurance |

| It is a life time comprehensive coverage that offers complete insurance. It pays out to your beneficiary at the point of the policy holder’s death. | These are medical coverage and covers health needs. It does not cover anything other than medical expenses. |

| It is a long-term plan. | It is a short-term plan. |

| The protection of the family and the dependants financially comes at the time of the demise of the policy holder. | This covers you and your family and takes care of your medical expenses during your life. |

Q27. What is the difference between primary and secondary data?

Ans.

| Primary Data | Secondary Data |

| Primary data are those that are collected for the first time. | Secondary data refer to those data that have already been collected by some other person. |

| These are in the form of raw materials. | These are in the finished form. |

| Collecting primary data is quite expensive both in the terms of time and money. | Secondary data requires less time and money; hence it is economical. |

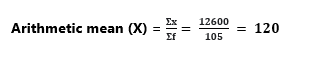

| x | f |

| 0 – 10 | 5 |

| 10 – 20 | 15 |

| 20 – 30 | 20 |

| 30 – 40 | 25 |

| 40 – 50 | 20 |

| 50 – 60 | 15 |

| 60 – 70 | 5 |

Q28. Calculate arithmetic mean from the data given below:

Ans.

| Marks | Mid Value (x) | Frequency (f) | (Fx) |

| 0 – 10 | 5 | 5 | 50 |

| 10 – 20 | 15 | 15 | 300 |

| 20 – 30 | 25 | 20 | 750 |

| 30 – 40 | 35 | 25 | 1400 |

| 40 – 50 | 45 | 20 | 2250 |

| 50 – 60 | 55 | 15 | 3300 |

| 60 – 70 | 65 | 5 | 4550 |

| Σf = 105 | Σx = 12600 |

Q29. Explain the role and importance of primary sector?

Ans. The importance of primary sector in our economy are as follow –

- Primary sector contributes more than 20% to the GDP of India.

- Its employment share is more than 55%.

- It is the most labouring sector of Indian economy.

- It covers agriculture, dairy, fishing, forestry which all contribute to the Indian economy.

Q30. What are the poverty alleviation programmes? Explain anyone.

Ans. Poverty Alleviation Programmes aims to reduce the rate of poverty in the country by providing proper access to food, monetary help, and basic essentials to the households and families belonging to the below the poverty line.

Jawahar Gram Samridhi Yojana (JGSY) – The Jawahar Rozgar Yojana (JRY) has been reorganized, streamlined, and expanded into the Jawahar Gram Samridhi Yojana (JGSY). It was established on April 1, 1999, with the goal of improving the quality of life of the rural poor by offering more productive work. India’s one major economic issue includes poverty. To combat the issue of poverty, the UPSC exam covers such topics as awareness and methods to alleviate poverty.

Q31. Distinguish between renewable and non-renewable resources. Give at least two examples of each.

Ans.

| Renewable Resources | Non-renewable Resources |

| Renewable resources cannot be depleted over time | Non-renewable resources deplete over time |

| Renewable resources include sunlight, water, wind and also geothermal sources such as hot springs and fumaroles. | Non-renewable energy includes fossil fuels such as coal and petroleum. |

| Most renewable resources have low carbon emissions and low carbon footprint. | Non-renewable energy has a comparatively higher carbon footprint and carbon emissions. |

| The upfront cost of renewable energy is high. – For instance, Generating electricity using technologies running on renewable energy is costlier than generating it with fossil fuels. | Non-renewable energy has a comparatively lower upfront cost. |

| Infrastructure for harvesting renewable energy is prohibitively expensive and not easily accessible in most countries. | Cost-effective and accessible infrastructure is available for non-renewable energy across most countries. |

| Requires a large land/ offshore area, especially for wind farms and solar farms. | Comparatively lower area requirements. |

Q32. Discuss in brief the rights of consumers in India?

Ans. The rights of consumers in India:

- Right to Safety

Means right to be protected against the marketing of goods and services, which are hazardous to life and property. The purchased goods and services availed of should not only meet their immediate needs, but also fulfil long term interests. - Right to be Informed

Means right to be informed about the quality, quantity, potency, purity, standard and price of goods so as to protect the consumer against unfair trade practices. - Right to Choose

Means right to be assured, wherever possible of access to variety of goods and services at competitive price. In case of monopolies, it means right to be assured of satisfactory quality and service at a fair price. It also includes right to basic goods and services. This is because unrestricted right of the minority to choose can mean a denial for the majority of its fair share. This right can be better exercised in a competitive market where a variety of goods are available at competitive prices. - Right to be Heard

Means that consumer’s interests will receive due consideration at appropriate forums. It also includes right to be represented in various forums formed to consider the consumer’s welfare. - Right to Seek redressal

Means right to seek redressal against unfair trade practices or unscrupulous exploitation of consumers. It also includes right to fair settlement of the genuine grievances of the consumer. - Right to Consumer Education

Means the right to acquire the knowledge and skill to be an informed consumer throughout life.Ignorance of consumers, particularly of rural consumers, is mainly responsible for their exploitation. They should know their rights and must exercise them. Only then real consumer protection can be achieved with success.